The Ultimate Relocation Guide: From Finding a House to Feeling at Home

The peak moving season is upon us. In fact, according to Move.com, almost 70% of U.S. moves occur between May and September.1 And while the percentage of Americans who move each year has declined, the desire to relocate remains strong.2,3

In fact, Architectural Digest recently declared “Americans are restless” after a survey found that 55% of adults “are moving, plan to move, or want to move” in 2024. The top reasons included: increased affordability; desire for safety; and closer proximity to work, family, or friends.3

If you’re one of those millions of Americans yearning for a change, this guide is for you.

Sure, moving can feel overwhelming, and it’s notoriously stressful. But, we’ve outlined six steps to make your move easier. Our hope is to alleviate some of the hassle of relocating—so you can focus on the adventure ahead!

- CHOOSE A COMMUNITY

When planning a relocation, one of the first things you’ll need to decide is where you want to live. This could be as broad as an area of town, or you might narrow it down to a specific neighborhood.

Depending on your priorities, you may want to start with communities that are close to work, friends, family and/or your preferred schools. If you commute, map out the route and check on the availability of public transportation, if you plan to use it. Then, if possible, try out the commute during rush hour to see what it’s like.

Next, it’s crucial to consider housing prices and cost of living so you don’t set your sights on an area that you can’t realistically afford. Don’t forget to look up local crime statistics to ensure the community is safe. Finally, visit any neighborhoods you’re considering to gauge the vibe and observe characteristics, like pedestrian accessibility, retail offerings, and population density.

Researching the ins and outs of various communities can be a time-consuming and sometimes difficult process, but we’re here to help! Give us a call to discuss your needs and aspirations, and we’d be happy to provide our recommendations of neighborhoods that may be a good fit for you.

- FIND YOUR NEW HOME

Once you’ve chosen an area to settle, the next decision you’ll need to make is whether you want to rent or buy a home. Renting can be a good option if you’re new to town, especially if you’re still saving up for a downpayment or you’re not ready to commit to a permanent location. Benefits include flexibility, less maintenance, and lower upfront costs.

But, if you want to avoid multiple moves—and you’re financially able—there’s no reason to delay the benefits of buying a home. Not only has homeownership been shown to increase your quality of life, but it’s also one of the best ways to protect and grow your wealth.4

The value of real estate will typically appreciate over time, and owners can build equity as they pay down their mortgage. Homeowners can also receive federal income tax deductions for mortgage interest and property taxes.

But, perhaps most importantly, homeownership offers stability. Property owners aren’t subject to the mercy of their landlords each year. According to Statista, average U.S. rental prices have risen more than 42% in the past 10 years.5 In contrast, a fixed-rate mortgage payment doesn’t rise at all.

If you decide to purchase a home and you choose us to represent you, you can rest easy knowing that we will be there for you throughout the entire journey, working hard to make the experience as easy and enjoyable as possible. Or, if you’re moving to a new area, we can refer you to a local agent in our network who shares our commitment to client service.

For more information about buying a home and a timeline of the home buying process, reach out to request a free copy of our Home Buyer’s Guide.

- SELL OR RENT OUT YOUR CURRENT HOME

If you already own a home, you’ll also need to start the process of either selling it or renting it out. We can help you evaluate your options based on current market conditions.

In many cases, our clients choose to sell so that they can use the equity in their current home to make a downpayment on their next one. But selling your home while simultaneously buying a new one can feel daunting to even the most seasoned homeowner.

Here are some of the most frequent concerns we hear from clients and our tips for addressing them:

- What will I do if I sell my house before I can buy a new one?

Check out furnished apartments, vacation rentals, and month-to-month leases. You may even find that a short-term rental arrangement can offer you an opportunity to get to know your new neighborhood better.

- What if I get stuck with two mortgages at the same time?

Ask us about contingencies that can be included in your contracts. For example, it’s possible to add a contingency to your purchase offer that lets you cancel the contract if you haven’t sold your previous home. We can discuss the pros and cons of these types of tactics and what’s realistic given the current market dynamics.

- What if I mess up my timing or burn out from all the stress?

Enlist support as early as possible. It’s our job to guide you and advocate on your behalf, so don’t be afraid to lean on us throughout the process. We’re here to ease your burden and make your move as seamless and stress-free as possible.

In addition to answering your questions, we’ll give you an idea of how much equity you have in your current home so you know how much you can afford to spend on your new one. Part of that process will include a plan to maximize your current home’s sale price. We utilize a proven strategy that’s designed to achieve an efficient sale while boosting your profits.

For a thorough breakdown of the technologies and marketing activities we use to get you the most money for your home sale, ask us for a copy of our Property Marketing Plan.

- PLAN YOUR DEPARTURE

Preparing for a move can be both exhilarating and exhausting. Fortunately, you don’t have to do everything in a day. You don’t have to do it all alone, either. When you work with us, we’ll be there every step of the way to help you navigate this process with ease. To that end, here are some of our top tips to help you plan for your departure.

If you have children, we typically advise that you start by sharing news about the move in an age-appropriate way. If possible, take them on a tour of your new home and neighborhood. This can alleviate some of the mystery and apprehension around the move. Don’t forget to contact their current and future schools, as well, to arrange for transfer and enrollment.

Next, you’ll want to start packing. To maintain order and make unpacking easier, we recommend packing one room at a time. Clearly label each box with its contents and the room it belongs to. And remember, there’s no use taking extraneous items with you. Use this opportunity to purge or donate possessions that you no longer need.

If you will be using a moving company, start researching and pricing your options. Make sure you’re working with a reputable service, and try to avoid paying a large deposit before your belongings are delivered. Once you have a moving date scheduled, you should arrange to have your utilities turned off or, if possible, transferred into the new homeowner’s name.

Finally, if you will be leaving friends or family behind, schedule get-togethers before your departure. The last days before moving can be incredibly hectic, so make sure you block off some time in advance for proper goodbyes.

Parting with a home and community you love can be hard, so try to stay focused on the exciting opportunities ahead. Feel free to reach out for referrals to moving companies, packing services, housekeepers, or any other resources that will make your move easier. We’d love to help.

- PREPARE FOR YOUR ARRIVAL

While it’s tempting to get wrapped up in the departure details, don’t forget to plan ahead for your arrival at your new home. To make your transition go smoothly, you should start preparing well before moving day. Here are a few pro tips to help you get started.

First, think about the utilities that will need to be turned on, especially essentials like water, electricity, and gas. Be sure to notify any relevant parties—banks, credit cards, subscriptions, etc.—about your change of address so you don’t miss any important bills, notices, or deliveries. You’ll also want to notify the postal service and submit a mail forwarding request.

If you plan to remodel, paint, or install new flooring, it’s often easier to have it done before you bring in all of your belongings. You may also want to have the house professionally cleaned before moving in.

Don’t forget about the items you’ll need (think toothbrush, towels, bedsheets) to make it through the first night in your new home. Designate some boxes with “Open Me First!” labels. (Pro tip: Keep a tool kit front and center for all that reassembling.)

Finally, create a list of all the restaurants you want to try and places you want to visit around your newly purchased home. Having a to-explore list keeps everyone’s spirits high and gives you starting points to settle into the neighborhood. If you’re relocating to our area, we can help! Reach out for a list of recommendations.

- GET SETTLED IN YOUR NEW SPACE

Studies show that moving can lead to feelings of loneliness and depression.6 However, there are ways to combat these negative effects. Here are a few strategies to help you and your family get settled in the new space.

If you have children, start by unpacking their rooms first. Seeing familiar items will help ease their transition and establish a “safe zone” where they can hang out away from the chaos of moving day. If possible, let them have a say in how their room is decorated.

Pets can also get overwhelmed by a new, unfamiliar space. Let them adjust to a single room first, which should include their favorite toys, treats, food and water bowl, and a litter box for cats. Once they seem comfortable, you can gradually introduce them to other rooms in the home.

Don’t forget to take care of yourself, too. Try to schedule breaks to get out of the house and investigate your new area. If you travel by foot or bicycle, you’ll gain the mood-boosting advantages of fresh air and exercise.

You can combat feelings of isolation by making an effort to meet people in your new community. Find a local interest group, take a class, join a place of worship, or volunteer for a cause. Don’t wait for friends to come knocking on your door. Instead, go out and find them.

To that end, make an effort to introduce yourself to your new neighbors, invite them over for coffee or dinner, and offer assistance when they need it. Once you’ve developed friendships and a support system within your new neighborhood, it will truly start to feel like home.

LET’S GET MOVING

While moving is never easy, these steps offer an action plan to get you started on your new adventure. With a little preparation—and the right team of professionals to assist you—it is possible to have a positive relocation experience.

We specialize in assisting home buyers and sellers with a seamless and “less-stress” relocation. Along with our referral network of moving companies, contractors, cleaning services, interior designers, and other home service providers, we can help take the hassle and headache out of your upcoming move. Give us a call or message us to schedule a free, no-obligation consultation!

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.

Sources:

- com –

https://www.moving.com/tips/12-tips-for-moving-during-peak-moving-season/

- com –

https://www.moving.com/tips/moving-trends-predictions-for-2024/

- Architectural Digest –

https://www.architecturaldigest.com/reviews/moving/moving-trends-survey

- National Association of Realtors –

https://www.nar.realtor/infographics/the-benefits-of-homeownership

- Statista –

https://www.statista.com/statistics/200223/median-apartment-rent-in-the-us-since-1980/

- Psychology Today –

https://www.psychologytoday.com/us/blog/is-where-you-belong/201607/why-youre-miserable-after-move

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

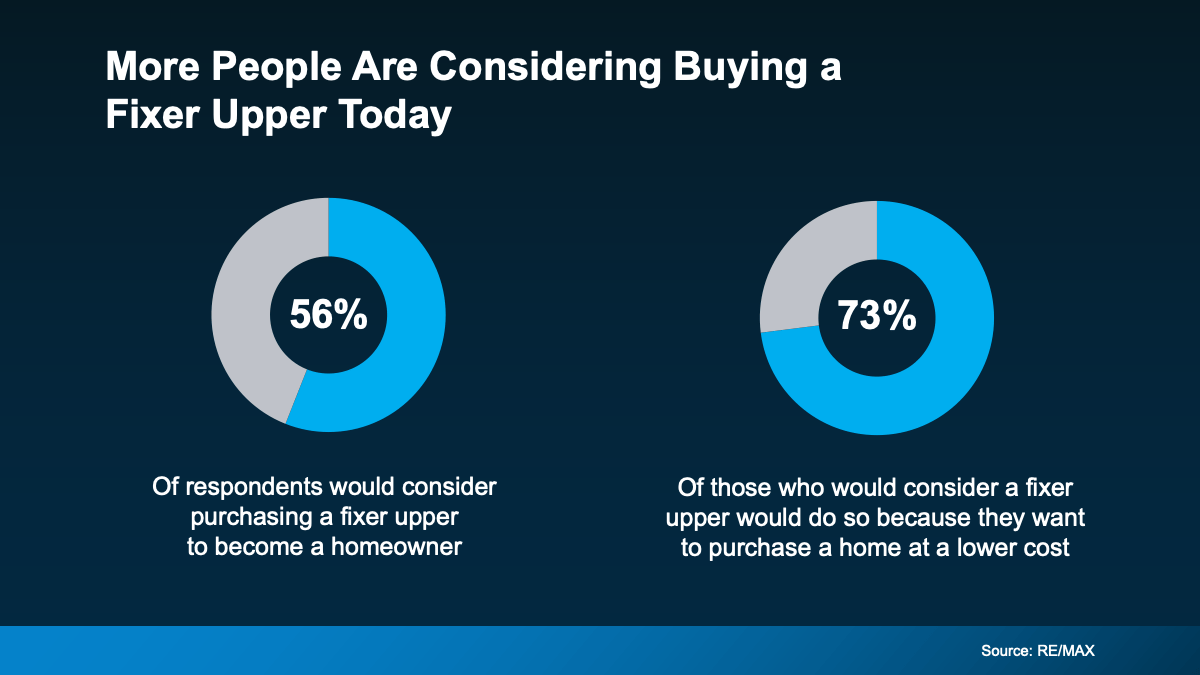

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

What This Means for You

What This Means for You